भारतीय banks और fintech apps के पास एक ऐसा problem है जिससे ज़्यादातर marketing teams jealous होंगी: users actually उनकी notifications सुनना चाहते हैं। UPI debit alert flash sale से बिल्कुल अलग land करता है। Low-balance warning open होती ही है। Challenge attention हासिल करना नहीं है — challenge उसे waste न करना है।

यह guide cover करती है कि banking और fintech apps में push notifications क्या करती हैं, कौन सी types real outcomes drive करती हैं, security और compliance कैसे handle करें, और Pushwoosh के साथ Indian market के लिए practical implementation कैसी दिखती है।

Banking में push notifications क्या हैं?

Banking push notification एक real-time message है जो user के mobile device पर उनके banking या fintech app के through deliver होता है। यह lock screen पर या notification center में दिखती है, app close होने पर भी — और internet के through Android पर Firebase Cloud Messaging (FCM) या iOS पर Apple Push Notification Service (APNs) के through deliver होती है। भारतीय context में FCM primary है क्योंकि Android की 95%+ market share है — entry-level devices (Xiaomi, Realme, Samsung Galaxy M-series, Vivo) पर stable FCM delivery business-critical है।

SMS के मुकाबले push notifications rich media, deep links और interactive action buttons support करती हैं। Email के मुकाबले seconds में पहुंचती हैं और inbox check की ज़रूरत नहीं। Banking में यह immediacy matter करती है: एक fraud alert जो 30 minutes late आता है, real-time वाले से completely अलग product है।

Financial services में push notifications दो functional categories में split होती हैं: transactional (UPI debit/credit, account activity, security alerts) और promotional (product offers, engagement nudges)। दोनों frequency, tone और compliance में अलग handling demand करती हैं।

भारतीय banking apps के लिए push क्यों matter करती है

Push उन few channels में से एक है जिनके पास mid-day user को interrupt करने का legitimate reason है। PhonePe, Paytm, Google Pay, HDFC, ICICI, SBI और Cred जैसे apps के पास यह permission है क्योंकि underlying need real है। सवाल यह है कि इसे well use करने के लिए infrastructure जगह पर है या नहीं।

Security और fraud prevention

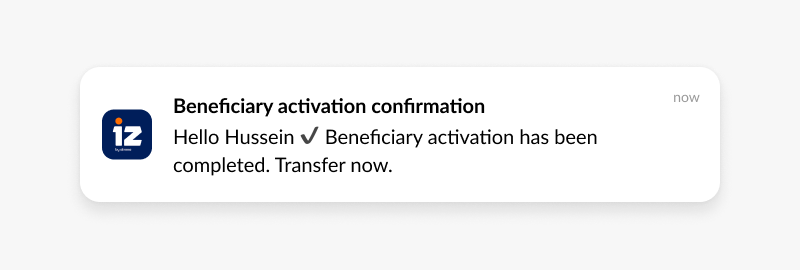

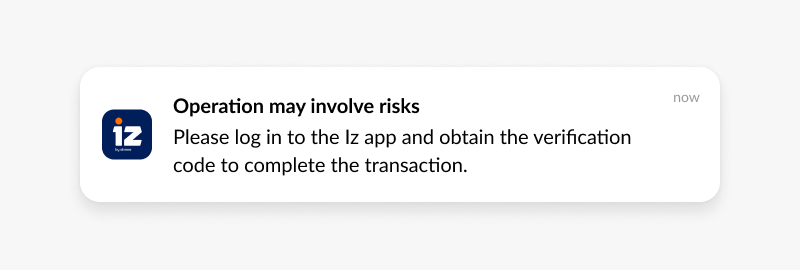

UPI transaction के 30 seconds बाद confirmation भेजना table stakes है। Higher-value use case anomaly detection है: नए device से login (देश के बाहर से या किसी नए शहर से), असामान्य amount का card-not-present transaction, password change। ये alerts users को real-time में activity confirm या deny करने का chance देते हैं — जिससे fraud window hours से seconds में compress हो जाती है।

Push-based multi-factor authentication (MFA) higher-security flows में SMS OTP को replace भी कर रही है। App के अंदर biometric confirmation — push से trigger — phone number पर भेजे गए code से ज़्यादा secure और faster है, जो SIM-swap हो सकता है (भारत में SIM-swap fraud एक growing concern है)।

Account activity और balance management

Low-balance alerts, salary credit notifications, bill payment reminders, EMI due dates और overdraft warnings high-utility notifications हैं जिन्हें users deliberately set up करते हैं। इनके opt-in rates किसी भी vertical में सबसे ज़्यादा होते हैं। Support call volume भी कम होती है: जिस user को real-time UPI payment confirmation मिल गया, वो “transaction successful हुआ या नहीं?” पूछने call नहीं करेगा।

Customer retention और CLV

जो users relevant, timely push notifications receive करते हैं वो longer active रहते हैं और non-subscribers से ज़्यादा revenue generate करते हैं। Mechanism complicated नहीं है: consistent, useful contact app खोलने की habit बनाता है। Push से शुरू होने वाला हर interaction financial relationship deepen करने का opportunity है।

Pushwoosh data Indian banking और neobanking apps में show करती है कि active push campaigns वाले users की 90-day retention non-subscribers से materially higher होती है, और CLV difference time के साथ compound होती है।

Product adoption और cross-sell

सही moment पर सही offer उस campaign से outperform करती है जो everyone को blast भेजी जाती है। एक user जिसने अभी अपना तीसरा international remittance complete किया है, वो forex card के लिए उस user से बेहतर candidate है जिसने पिछले 30 days में कोई transaction नहीं किया। Behavioral segmentation यह gap close करती है।

Indian financial services में push notifications के types

हर notification type customer lifecycle में distinct purpose serve करती है। Type सही करना उतना ही important है जितना copy सही करना।

Transactional notifications

Account activity के real-time confirmations। ये banking में highest-trust notifications हैं क्योंकि ये वो information carry करती हैं जिसका users actively wait कर रहे होते हैं।

- “₹2,499 का payment Swiggy को process हो गया। UPI Ref: 412345678901”

- “₹45,000 — Acme Pvt Ltd से salary आपके HDFC account में credit हो गई।”

- “आपके credit card का ₹8,750 का bill 3 दिन में due है।“

Security alerts

Time-sensitive notifications जो users को fast act करने empower करती हैं। Copy direct होनी चाहिए, action button obvious, और deep link immediate।

- “नए device से login (iPhone 14, Bengaluru). अगर यह आप नहीं थे, account secure करने tap करें।”

- “₹15,000 का transaction — Tanishq, Mumbai। क्या यह आप थे?”

- “आपका password change हुआ है। यह आप नहीं थे? हमसे अभी contact करें।“

Informational updates

App changes, maintenance windows, policy updates, RBI guideline updates। ये factual और short होनी चाहिए। Users entertainment के लिए नहीं पढ़ते — वो check करते हैं कि कुछ उन्हें affect करता है या नहीं।

- “नए budgeting tools app में live हैं। Smart spending insights explore करें।”

- “Scheduled maintenance: app 2-4 AM IST, 26 October को offline रहेगा।“

Promotional notifications

Offers, product launches, rate changes। इनकी irrelevance tolerance सबसे कम है। Savings rate offer एक ऐसे user को जिसके पास already ₹2 Lakh का savings balance है, relevant है। वही offer एक नए user को जिसने अभी तक deposit नहीं किया, noise है।

- “Savings पर 7.5% interest unlock करें — limited-time offer।”

- “Platinum Rewards में upgrade करें: travel पर 3x reward points।”

- “मिनटों में low-interest personal loan के लिए pre-approved हों।“

Behavioral और personalized notifications

Specific user actions या inactivity से triggered। इनकी CTR किसी भी notification type की highest होती है क्योंकि ये तब arrive करती हैं जब user का context message को meaningful बनाता है।

- “आपका checking balance ₹500 से नीचे है। Overdraft fees से बचने के लिए funds transfer करें।”

- “आपने इस महीने Zomato और Swiggy पर पिछले से ज़्यादा spend किया। Spending report देखें।”

- “आप अपने Goa trip savings goal से ₹5,000 दूर हैं।“

Indian banking और fintech में push notification use cases

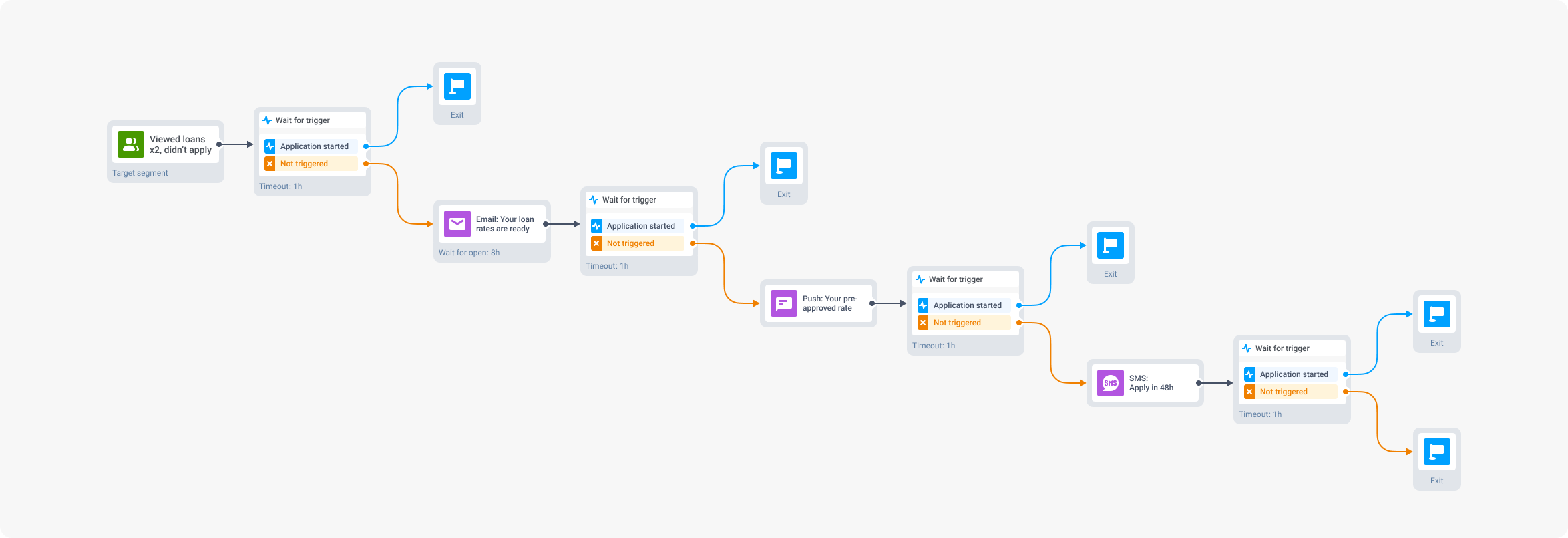

नए users का onboarding

ज़्यादातर app installs जो पहले 72 hours में convert नहीं होते, कभी convert नहीं होते। Push notifications वही एक channel हैं जो new user तक app के बाहर पहुंचकर उन्हें setup steps के through move करते हैं। यह विशेष रूप से PhonePe, Paytm, Cred, Slice, Jupiter, Fi और Niyo जैसे fintech apps के लिए critical है जहां daily user acquisition lakhs में होती है।

- Day 1: “[Bank] में स्वागत है। सभी features unlock करने के लिए profile complete करें।”

- Day 2 (profile incomplete): “बस कुछ steps बाकी हैं। Finish करने tap करें।”

- Day 3 (still incomplete): “पहली UPI transaction complete करें और ₹100 का cashback पाएं।”

हर step तभी send होता है जब पिछला convert नहीं हुआ। Pushwoosh का Customer Journey Builder इस conditional logic को बिना code के visually handle करता है।

Fraud detection और security alerts

Suspicious activity detected होने पर seconds में push निकलता है, दो action buttons के साथ: Confirm और Deny। Deny tap करना सीधे card-lock screen पर deep-link करता है। Fraud और user response के बीच का window hours से एक minute से कम हो जाता है।

- Event: Card किसी unusual merchant या location पर use हुआ।

- Push: “₹12,500 — [Merchant]। क्या यह आप थे?” + Confirm / Report Fraud buttons।

- Deny path: Card lock करने और support contact के लिए immediate deep-link।

Account activity management

Balance alerts, UPI payment confirmations और overdraft warnings users खुद set up करते हैं। ये सही करना सबसे easy notifications में हैं: user ने आपको बताया है कि वो क्या जानना चाहते हैं, तो वही बताइए। UPI Lite transactions, RuPay card spends और Aadhaar-linked direct benefit transfers — सबको real-time confirmation मिलनी चाहिए।

Loan और product abandonment recovery

जिस user ने loan application शुरू की और रुक गया, वो warm lead है — cold नहीं। उन्होंने already intent express किया है। 24 hours बाद targeted push किसी भी cold prospects को target करने वाली acquisition campaign से meaningfully higher rate पर convert करती है। Indian fintech में personal loan, credit card और BNPL applications के लिए यह pattern विशेष रूप से strong है।

Win-back campaigns

जो users 30+ days से transact नहीं किए उन्हें वापस आने का reason चाहिए जो उनके लिए specific हो, generic नहीं। RFM segmentation identify करती है कि कौन से dormant users targeting worth हैं (वो जो quiet होने से पहले high-value थे) और उस segment के लिए कैसा incentive sense रखता है।

Personalized financial guidance

Frequent travelers identified users को forex card offers मिलते हैं। पिछले हफ्ते investment tab तीन बार खोलने वाले users को “ready to get started?” nudge। Segmentation सारा काम करती है — push सिर्फ delivery mechanism है।

Security, privacy और compliance

यह वो section है जो ज़्यादातर push documentation gloss over करती है। Financial institutions के लिए यह footnote नहीं होनी चाहिए।

Data handling

Push notification payloads में sensitive account data नहीं होना चाहिए। Full account numbers, card numbers, complete balances notification preview में नहीं belong करते। Secure deep link use करें जो app के authenticated section की ओर ले जाए, जहां users biometric verification के बाद details देख सकें। Notification में क्या जाता है: reference number, transaction amount, merchant name। App में क्या रहता है: बाकी सब कुछ।

Transit में data TLS 1.2 या higher से encrypted होना चाहिए। Rest में data को equivalent protection चाहिए। यह device tokens, user identifiers और engagement platform में stored notification content पर apply होता है।

Consent और opt-in management

Push notification consent के regulatory requirements region और notification type से vary करते हैं। Transactional alerts अक्सर GDPR के तहत legitimate interest या contractual necessity के तहत qualify करते हैं, लेकिन promotional notifications को ज़्यादातर jurisdictions में explicit opt-in चाहिए। भारत में India’s Digital Personal Data Protection Act (DPDP Act) के तहत consent management framework evolve हो रहा है — granular control build करना आगे की compliance के लिए future-proof approach है।

Users को granular control चाहिए: fraud alerts receive करने की ability without promotional messages। Notification preference management app में build करें, settings में buried नहीं। जो users control कर सकते हैं वो entirely opt out करने की कम likely होते हैं।

Regulatory frameworks

| Regulation | Scope | Push के लिए Relevance |

|---|---|---|

| GDPR | EU users | Promotional push के लिए explicit consent; withdraw करने का right; payloads में data minimization |

| CCPA | California residents | Data sharing से opt out का right; disclosure requirements |

| PCI DSS | Cardholder data | Card numbers, CVVs और auth codes notification content में नहीं appear होने चाहिए |

| India's DPDP Act (context) | Indian users | Notice और consent requirements; data fiduciary obligations। Pushwoosh DPDP-specific certification claim नहीं करता। |

Pushwoosh audit logs, data processing agreements और flexible consent management tooling provide करता है ताकि उपरोक्त सब के साथ compliance support हो। Note: Pushwoosh SOC 2 Type I, ISO 27001:2022, HIPAA और GDPR certified है। EU और US data centers। Pushwoosh RBI compliance, DPDP Act compliance या किसी Indian regulator-specific certification का दावा नहीं करता।

Indian banking push notifications के लिए best practices

Opt-in flow में transactional को promotional से अलग करें

अगर आप एक single blanket notification permission मांगते हैं, तो आप एक promotional mis-fire से fraud alert delivery खोने के एक step दूर हैं। Notification categories को start से segment करें: security alerts, account activity और promotional offers independent opt-ins होने चाहिए। Promotions से opt out करने वाले users को भी fraud alerts मिलने चाहिए।

Personalize करें या भेजें ही नहीं

Average Indian banking user gaming user से higher notification frequency tolerate कर सकता है, लेकिन सिर्फ तब जब messages relevant हों। ₹0 savings balance वाले user को savings rate offer सिर्फ irrelevant नहीं — trust को damage करती है। Behavioral segmentation और RFM targeting exactly इसी को prevent करने के लिए हैं।

Volume से ज़्यादा timing matters

Per-user optimal timing consistently fixed-time sends से outperform करती है। Pushwoosh का Best Time to Send हर user का historical engagement pattern analyze करता है और messages तब deliver करता है जब वो open करने की most likely हो। Banking में यह promotional content के लिए विशेष रूप से relevant है: एक loan offer जो user के actively finances manage करते समय arrive करती है, उससे different rate पर convert करती है जो Sunday सुबह 6 AM पर arrive करती है। Indian context में office commute hours (8-10 AM, 6-9 PM IST) historically high-engagement windows हैं।

Texting जैसे लिखें, report file नहीं कर रहे

Bank copy formal की तरफ tend करती है। Push notifications इसके opposite होनी चाहिए: short, direct, clear। बताएं क्या हुआ। बताएं user को क्या करना चाहिए। हर word remove करें जो इन दो things में contribute नहीं करता। “आपके account पर एक बड़ा transaction detect हुआ है। कृपया review करें” दस words ज़्यादा है। “₹15,000 — Tanishq Mumbai। क्या यह आप थे?” वही information छह words में।

हर segment अलग test करें

जो subject line high-value active users के लिए काम करती है वो dormant users पर differently perform करती है। Promotional content के लिए जो urgency frame action drive करती है, security context में alarming feel कर सकती है। A/B tests segments के भीतर run करें, full user base पर नहीं — और downstream conversion measure करें, सिर्फ CTR नहीं।

Pushwoosh कैसे Indian banking और fintech teams को support करता है

Fintech और banking apps के पास ऐसी requirements हैं जिनके लिए generic engagement platforms नहीं बने थे: real-time event triggers, granular segmentation, compliance infrastructure और scale पर delivery reliability। Pushwoosh इन सब के लिए built है — और भारतीय market की unique scale demands (PhonePe, Paytm scale पर crore-level DAU) के लिए battle-tested।

- Real-time event triggers — transaction events, login signals और behavioral flags को instant push delivery से connect करें। Fraud alerts seconds में निकलते हैं, minutes में नहीं।

- Customer Journey Builder — onboarding sequences, abandonment recovery और win-back flows के लिए visual, no-code automation — push, in-app, email और SMS पर।

- Behavioral segmentation और RFM — users को इस आधार पर segment करें कि उन्होंने क्या किया, सिर्फ कौन हैं इस पर नहीं। High-value dormant users को नए users से different treatment मिले।

- Dynamic content personalization — real-time account data, transaction details और user attributes सीधे notification copy में pull करें (₹ amounts, UPI references, merchant names)।

- Compliance tooling — audit logs, data processing agreements, granular opt-in management और GDPR/CCPA-ready data handling।

- Android-first delivery reliability — Indian device landscape (Xiaomi, Realme, Vivo, Samsung Galaxy M-series) पर aggressive battery optimization के बावजूद stable FCM delivery।

- ManyMoney AI — उन users को identify करता है जो product offers पर convert होने की most likely हैं, churn risk को churn बनने से पहले flag करता है, और bina manual configuration के campaign timing optimize करता है।

FinTech और banking solution page explore करें या Pushwoosh को action में नीचे देखें।