Bank-এর একটা সমস্যা আছে যা বেশিরভাগ marketing team-এর কাছে enviable: user-রা সত্যিই bank থেকে শুনতে চায়। একটা fraud alert flash sale-এর মতো ignore হয় না। Low-balance warning open হয়। চ্যালেঞ্জ attention পাওয়া নয় — চ্যালেঞ্জ সেটা waste না করা।

বাংলাদেশের context-এ ব্যাপারটা আরো sharp। দেশটা mobile-first by necessity: smartphone penetration প্রতি বছর বাড়ছে, প্রায় ৯৫%+ device Android, এবং একটা পুরো generation প্রথম “bank account” হিসেবে bKash বা Nagad app-কে চেনে। এই reality-তে push notification শুধু একটা channel না — এটাই প্রায়ই আপনার সাথে user-এর primary touchpoint।

এই গাইডে: banking ও fintech app-এ push notification আসলে কী করে, কোন type-গুলো সত্যিই কাজে আসে, security ও compliance কীভাবে handle করবেন, এবং Pushwoosh দিয়ে practical implementation কেমন দেখায়।

Banking-এ push notification কী?

Banking push notification মানে user-এর mobile device-এ real-time delivered একটা message — তার banking বা fintech app-এর মাধ্যমে। App বন্ধ থাকলেও এটা lock screen বা notification center-এ দেখা যায়, এবং internet-এর মাধ্যমে delivered হয় iOS-এ Apple Push Notification Service (APNs) দিয়ে, আর Android-এ Firebase Cloud Messaging (FCM) দিয়ে।

SMS-এর থেকে আলাদা: push notification rich media, deep link (অর্থাৎ direct app-এর নির্দিষ্ট page-এ নিয়ে যাওয়া link), এবং interactive action button support করে। Email-এর থেকে আলাদা: এটা কয়েক second-এর মধ্যে পৌঁছায়, inbox check করার দরকার নেই। Banking-এ এই immediacy-টাই key — ৩০ minute late আসা fraud alert কার্যত একটা আলাদা product, real-time alert-এর তুলনায়।

বাংলাদেশের mobile financial services (MFS) ecosystem — bKash, Nagad, Rocket (DBBL), Upay, Tap (City Bank), MyCash — দেখলে এটা পরিষ্কার হয়। কোটি user এই app-গুলো থেকে দিনে multiple push পায়: cash-in confirmation, send money receipt, merchant payment, mobile recharge। SMS এই scale-এ unsustainable হতো — push এই entire experience-কে possible করেছে।

Financial services-এ push notification দুই functional category-তে ভাগ হয়: transactional (account activity, security alert) এবং promotional (product offer, engagement nudge)। দুটোর frequency, tone ও compliance handling আলাদা হওয়া দরকার।

Banking app-এ push notification কেন গুরুত্বপূর্ণ

Push হচ্ছে সেই অল্প কয়েকটা channel-এর একটা যেগুলোর user-কে দিনের মাঝখানে interrupt করার legitimate reason আছে। Bank-এর সেই permission আছে কারণ underlying need আসলেই real। প্রশ্ন হচ্ছে — সেটাকে ভালোভাবে ব্যবহার করার infrastructure আছে কিনা।

Security ও fraud prevention

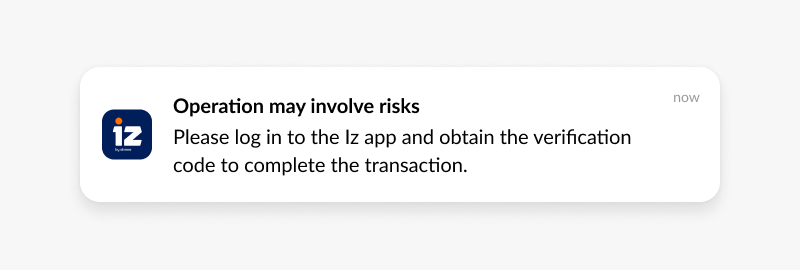

Purchase-এর ৩০ second পরে আসা transaction confirmation — এটা এখন bare minimum। আসল high-value use case হলো anomaly detection: নতুন device থেকে login, ভিন্ন দেশ থেকে access, অস্বাভাবিক amount-এর card-not-present transaction, password change। এই alert-গুলো user-কে real-time-এ activity confirm বা deny করার সুযোগ দেয় — fraud window ঘণ্টা থেকে কয়েক second-এ নেমে আসে।

Push-based multi-factor authentication (MFA) higher-security flow-এ SMS OTP-কে replace করছে। App-এর ভেতরে biometric confirmation, একটা push দিয়ে triggered — এটা SMS OTP-এর চেয়ে দ্রুত এবং বেশি secure, কারণ SIM-swap fraud বাংলাদেশে real concern।

Account activity ও balance management

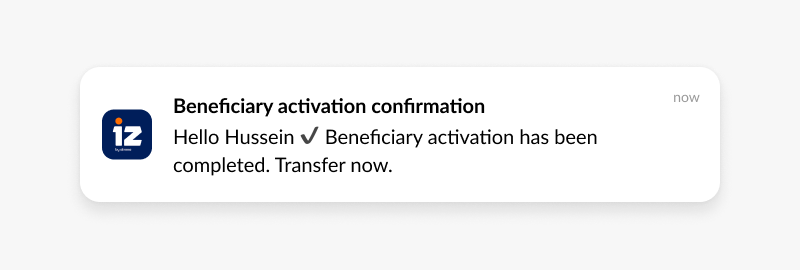

Low-balance alert, salary credit, bill payment reminder, overdraft warning — এই notification user নিজে deliberately set up করে। যেকোনো vertical-এ এই type-এর opt-in rate সবচেয়ে বেশি। এগুলো support call volume-ও কমায়: যে user real-time payment confirmation পেয়ে যায়, সে call করে জিজ্ঞেস করে না “টাকাটা গেলো কিনা।”

বাংলাদেশে এটা আরো গুরুত্বপূর্ণ — gas bill, electricity bill, internet bill সব এখন bKash/Nagad/Rocket দিয়ে pay হয়। প্রতিটা successful transaction-এর instant confirmation user-এর trust-এর foundation।

Customer retention ও CLV

যে user relevant, timely push notification পায় সে inactive user-দের চেয়ে long-term-এ বেশি active থাকে এবং বেশি revenue generate করে। Mechanism জটিল না: consistent, useful contact app খোলার habit তৈরি করে। প্রতিটি push-দিয়ে শুরু হওয়া interaction একটা financial relationship-কে গভীর করার সুযোগ।

Pushwoosh-এর banking app data দেখায়, active push campaign-এ থাকা user-রা non-subscriber-দের তুলনায় significantly higher 90-day retention দেখায়, এবং CLV-এর difference সময়ের সাথে cumulative ভাবে বাড়ে।

Product adoption ও cross-sell

সঠিক offer সঠিক moment-এ সবার কাছে blast পাঠানোর চেয়ে অনেক ভালো কাজ করে। যে user সবেমাত্র তৃতীয় international remittance complete করেছে (বাংলাদেশের context-এ গুরুত্বপূর্ণ — remittance বড় economic flow), সে travel card বা forex card-এর জন্য ভালো candidate — তুলনায় যে ৩০ দিন transact করেনি তার চেয়ে। Behavioral segmentation (অর্থাৎ user কী করেছে তার ভিত্তিতে group তৈরি) এই gap বন্ধ করে।

Financial services-এ push notification-এর type

প্রতিটি notification type customer lifecycle-এ একটা আলাদা purpose serve করে। সঠিক copy লেখার মতোই সঠিক type বাছাই করাও গুরুত্বপূর্ণ।

Transactional notification

Account activity-র real-time confirmation। Banking-এ এগুলোই highest-trust notification, কারণ user actively এই information-এর জন্য অপেক্ষা করছে।

- “Acme Corp.-এ ৳১৫,০০০ payment successful। Ref: #12345”

- “Payroll Solutions থেকে ৳৪৫,০০০ আপনার account-এ credited হয়েছে।”

- “আপনার electricity bill ৳২,৩০০ ৩ দিন পর due।“

Security alert

Time-sensitive notification যা user-কে দ্রুত action নিতে সাহায্য করে। Copy direct হতে হবে, action button পরিষ্কার, এবং deep link instant।

- “নতুন device থেকে login (iPhone 14, ঢাকা)। আপনি না হলে tap করে account secure করুন।”

- “Luxury Goods Store-এ ৳৭৫,০০০ — এটা কি আপনি?”

- “আপনার password change হয়েছে। আপনি করেননি? এখনই contact করুন।“

Informational update

App change, maintenance window, policy update। এগুলো factual ও short হতে হবে। User entertainment-এর জন্য পড়ে না; পড়ে এটা জানার জন্য যে এটা তাকে affect করে কিনা।

- “App-এ নতুন budgeting tool live। Smart spending insights explore করুন।”

- “Scheduled maintenance: ২৬/১০ রাত ২-৪টা পর্যন্ত app offline থাকবে।“

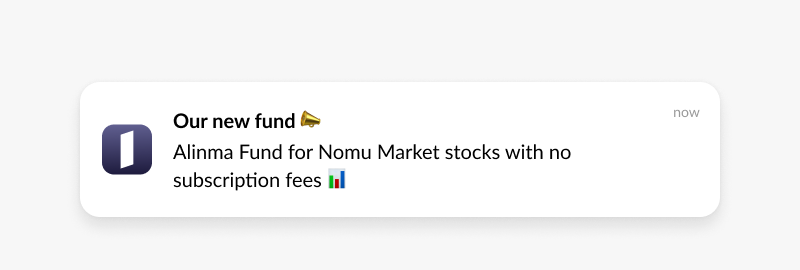

Promotional notification

Offer, product launch, rate change। এগুলোতে irrelevance-এর tolerance সবচেয়ে কম। Savings account-এ balance থাকা user-কে savings rate offer relevant; কিন্তু যে user এখনো প্রথম deposit করেনি তার কাছে একই offer হলো noise — বা আরো খারাপ, trust damage।

- “আপনার DPS-এ ৮.৫% interest unlock করুন — limited-time offer।”

- “Platinum Rewards-এ upgrade করুন: travel-এ 3x point।”

- “কয়েক minute-এ low-interest auto loan-এর জন্য pre-approved হোন।“

Behavioral ও personalized notification

Specific user action বা inactivity দিয়ে triggered। এগুলোর CTR সব type-এর মধ্যে সবচেয়ে বেশি — কারণ user-এর current context-এ message-টা meaningful।

- “আপনার checking balance ৳১,০০০-এর নিচে। Overdraft fee এড়াতে fund transfer করুন।”

- “এই মাসে আপনি গত মাসের চেয়ে dining-এ বেশি spend করেছেন। Spending report দেখুন।”

- “আপনি travel savings goal থেকে ৳৫,০০০ দূরে।“

Banking push notification-এর use case

নতুন user-দের onboarding

বেশিরভাগ app install যেগুলো প্রথম ৭২ ঘণ্টায় convert হয় না, সেগুলো আর কখনো convert হয় না। Push notification-ই একমাত্র channel যা নতুন user-কে app-এর বাইরে থেকে reach করে setup step-গুলোর মধ্য দিয়ে move করায়।

- Day 1: “[Bank]-এ স্বাগতম। সব feature unlock করতে profile complete করুন।”

- Day 2 (profile incomplete): “মাত্র কয়েকটা step বাকি। শেষ করতে tap করুন।”

- Day 3 (still incomplete): “প্রথম deposit complete করুন এবং ৳৫০০ bonus পান।”

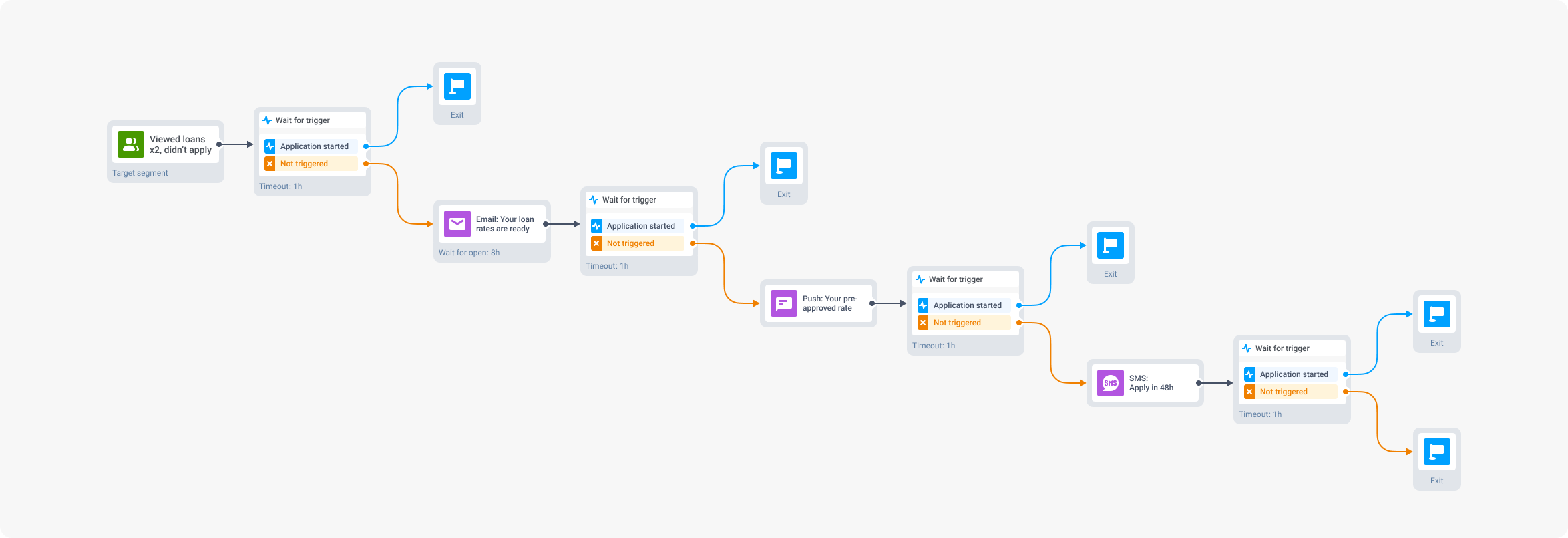

প্রতিটি step শুধু তখনই পাঠানো হয় যখন আগেরটা convert হয়নি। Pushwoosh-এর Customer Journey Builder (অর্থাৎ visual flow editor যেখানে if-then logic ছাড়াই কোনো code লিখতে হয় না) এই conditional logic visually handle করে।

Fraud detection ও security alert

Suspicious activity detect হওয়া মানে কয়েক second-এর মধ্যে push চলে যায়, দুটো action button সহ: Confirm এবং Deny। Deny tap করলে direct card-lock screen-এ deep-link নিয়ে যায়। Fraud এবং user response-এর মধ্যের window ঘণ্টা থেকে এক minute-এর নিচে নেমে আসে।

- Event: অস্বাভাবিক merchant বা location-এ card use।

- Push: “[Merchant]-এ ৳৫০,০০০ — এটা কি আপনি?” + Confirm / Report Fraud button।

- Deny path: card lock করতে এবং support contact করতে immediate deep link।

Account activity management

Balance alert, payment confirmation, overdraft warning — এগুলো user নিজেই set up করে যারা এই information চায়। এগুলো সবচেয়ে easy-to-get-right notification: user আপনাকে বলে দিয়েছে সে কী জানতে চায়, তাই সেটাই বলুন।

Loan ও product abandonment recovery

যে user loan application শুরু করে স্থগিত করেছে সে cold lead না — warm lead। সে intent already express করেছে। ২৪ ঘণ্টা পরে targeted push cold prospect-কে target করা যেকোনো acquisition campaign-এর চেয়ে meaningfully higher rate-এ convert করে।

Win-back campaign

যে user ৩০+ দিনে transact করেনি তাকে ফিরিয়ে আনতে generic না, specific reason লাগে। RFM segmentation (Recency, Frequency, Monetary value-এর ভিত্তিতে user grouping — অর্থাৎ কে সম্প্রতি কতবার এবং কত টাকার transaction করেছে) identify করে কোন dormant user target করার মতো (যারা চুপ হওয়ার আগে high-value ছিল) এবং সেই segment-এর জন্য কী incentive sense করে।

Personalized financial guidance

Frequent traveler হিসেবে identified user-রা travel card offer পান। যে user গত সপ্তাহে investment tab তিনবার খুলেছে সে “শুরু করতে ready?” nudge পায়। Segmentation কাজ করে; push শুধু delivery mechanism।

Security, privacy ও compliance

এই section বেশিরভাগ push documentation-এ skim করে চলে যায়। Financial institution-এর জন্য এটা footnote হওয়া উচিত না।

Data handling

Push notification payload-এ sensitive account data থাকা উচিত না। সম্পূর্ণ account number, card number, balance — এগুলো notification preview-তে থাকার জায়গা না। একটা secure deep link ব্যবহার করুন যা app-এর authenticated section-এ নিয়ে যায়, যেখানে biometric verification-এর পর user details দেখতে পারে। Notification-এ যা থাকতে পারে: একটা reference number, transaction amount, merchant name। App-এ যা থাকবে: বাকি সব।

Transit-এ থাকা সব data TLS 1.2 বা উপরের version দিয়ে encrypted হতে হবে। Rest-এ থাকা data-র জন্যও equivalent protection দরকার। এটা device token, user identifier, এবং engagement platform-এ stored notification content — সবার জন্য প্রযোজ্য।

Consent ও opt-in management

Push notification consent-এর regulatory requirement region ও notification type অনুযায়ী আলাদা। Transactional alert প্রায়ই GDPR-এর অধীনে legitimate interest বা contractual necessity-র আওতায় পড়ে, কিন্তু promotional notification-এর জন্য বেশিরভাগ jurisdiction-এ explicit opt-in দরকার।

User-কে granular control দিতে হবে: fraud alert পাওয়া যাবে কিন্তু promotional message পাওয়া যাবে না — এই option থাকতে হবে। Notification preference management app-এ build করুন, settings-এ deep buried না। যে user control করতে পারে সে entirely opt-out করার সম্ভাবনা কম।

Regulatory framework

| Regulation | Scope | Push-এর সাথে relevance |

|---|---|---|

| GDPR | EU user | Promotional push-এর জন্য explicit consent; withdrawal-এর অধিকার; payload-এ data minimization |

| CCPA | California resident | Data sharing থেকে opt-out-এর অধিকার; disclosure requirement |

| PCI DSS | Cardholder data | Card number, CVV, auth code notification content-এ থাকতে পারবে না |

| FFIEC guidance | US financial institution | Technology risk management; third-party platform-এর জন্য vendor oversight |

Pushwoosh audit log, data processing agreement, এবং flexible consent management tooling provide করে যা উপরের সবগুলোর সাথে compliance support করে।

Banking push notification-এর best practice

Opt-in flow-এ transactional ও promotional আলাদা রাখুন

আপনি যদি একটাই blanket notification permission চান, তাহলে একটা promotional mis-fire-এর দূরত্বে আপনি fraud alert delivery হারাতে পারেন। শুরু থেকেই notification category segment করুন: security alert, account activity, এবং promotional offer — তিনটে independent opt-in হওয়া উচিত। Promotion থেকে opt-out করা user-রাও fraud alert পেতে থাকবেন।

Personalize করুন, না হলে পাঠাবেন না

Average banking user gaming user-এর চেয়ে higher notification frequency tolerate করতে পারে, কিন্তু শুধু যদি message-গুলো relevant হয়। Zero savings balance-এ থাকা user-কে savings rate offer পাঠানো শুধু irrelevant না — এটা trust damage করে। Behavioral segmentation ও RFM targeting ঠিক এটা prevent করার জন্যই আছে।

Time volume-এর চেয়ে বেশি matter করে

Per-user optimal timing consistently fixed-time send-কে outperform করে। Pushwoosh-এর Best Time to Send (অর্থাৎ প্রতিটি user-এর historical engagement pattern analyze করে individual basis-এ সেরা send time বের করা) প্রতিটি user-এর pattern analyze করে এবং যখন তারা সবচেয়ে বেশি open করার সম্ভাবনা সেই সময়ে message deliver করে। Banking-এ এটা বিশেষভাবে relevant promotional content-এর জন্য: যে loan offer user-এর finance manage করার সময় arrive করে সেটা Sunday সকাল ৬টায় আসা offer-এর চেয়ে আলাদা rate-এ convert করে।

Report file করছেন না, text করছেন — সেভাবেই লিখুন

Bank-এর copy formal হওয়ার দিকে ঝোঁকে। Push notification-এর হওয়া দরকার ঠিক উল্টো: short, direct, clear। কী হয়েছে state করুন। User-এর কী করা উচিত state করুন। যে word এই দুটোতে contribute করছে না সেটা বাদ দিন। “আপনার account-এ একটি বড় transaction detected হয়েছে। দয়া করে review করুন” — দশটা word বেশি। “Luxury Goods-এ ৳৭৫,০০০ — এটা কি আপনি?” — same information, ছয়টা word-এ।

প্রতিটি segment আলাদা test করুন

High-value active user-দের জন্য কাজ করা subject line dormant user-দের জন্য আলাদা perform করে। Promotional content-এ action drive করা urgency frame security context-এ alarming feel করতে পারে। A/B test segment-এর ভেতরে চালান, পুরো user base জুড়ে না — এবং downstream conversion measure করুন, শুধু CTR না।

Pushwoosh কীভাবে banking ও fintech team-কে support করে

Fintech ও banking app-এর এমন requirement আছে যেগুলোর জন্য generic engagement platform built না: real-time event trigger, granular segmentation, compliance infrastructure, এবং scale-এ delivery reliability। Pushwoosh এই সবের জন্য তৈরি।

- Real-time event trigger — transaction event, login signal, এবং behavioral flag-কে instant push delivery-র সাথে connect করুন। Fraud alert কয়েক second-এ যায়, minute-এ না।

- Customer Journey Builder — onboarding sequence, abandonment recovery, এবং win-back flow-এর জন্য visual, no-code automation — push, in-app, email ও SMS-এর across।

- Behavioral segmentation ও RFM — user-রা কী করেছে তার ভিত্তিতে segment করুন, শুধু তারা কে তার ভিত্তিতে না। High-value dormant user নতুন user-দের চেয়ে আলাদা treatment পায়।

- Dynamic content personalization — real-time account data, transaction detail, এবং user attribute সরাসরি notification copy-তে pull করুন।

- Compliance tooling — audit log, data processing agreement, granular opt-in management, এবং GDPR/CCPA-ready data handling।

- ManyMoney AI — product offer-এ convert করার সম্ভাবনা সবচেয়ে বেশি এমন user-দের identify করে, churn হওয়ার আগে churn risk flag করে, এবং manual configuration ছাড়াই campaign timing optimize করে।

Fintech ও banking solution page explore করুন, বা নিচে Pushwoosh কাজ করতে দেখুন।